Africa's FMCG Sector has become the World's Most Exciting Frontier

A research-backed guide for entrepreneurs, investors and brand builders entering the African FMCG market

The $1 Trillion Opportunity: How Africa's FMCG Sector Became the World's Most Exciting Frontier

A Djula Trader's Inventory, Circa 1350 AD

Long before anyone coined the phrase "fast-moving consumer goods," a network of merchants called the Dyula (also written Djula or Wangara) had already mastered its core principle: sell what people need every single day, move it fast, and build your routes wider than your rivals could imagine.

Originating in the Mande-speaking regions of West Africa, the Dyula traders of the 13th and 14th centuries ran what was arguably the continent's first FMCG empire. From the salt mines of Taghaza in the Sahara to the gold and kola nut markets of the forest belt, they traded the consumables of their time - commodities consumed quickly, replenished constantly, and demanded by every household regardless of income. Salt preserved food, kola nuts stimulated labour and marked social ceremony, cloth covered bodies, and millet fed cities. These were not luxuries. These were the everyday essentials of a civilization.

The Dyula did not just trade. They built distribution systems. They established credit networks. They understood local consumer preferences in every market they entered. A Dyula merchant operating in Djenné would know which flavour of kola - the bitter Ghanaian or the sweeter Nigerian variety - his buyers preferred, and he would price accordingly. He understood that branding, even in pre-modern form, mattered: his reputation, his relationships, and his reliability were his brand equity.

Centuries later, the fundamental logic of their trade has not changed. Across Africa today, the same imperatives drive the FMCG sector: understand the consumer, solve the distribution problem, price for the market, and build trust. What has changed is the scale, the speed, and the staggering size of the prize.

The Scale of What's Actually Happening

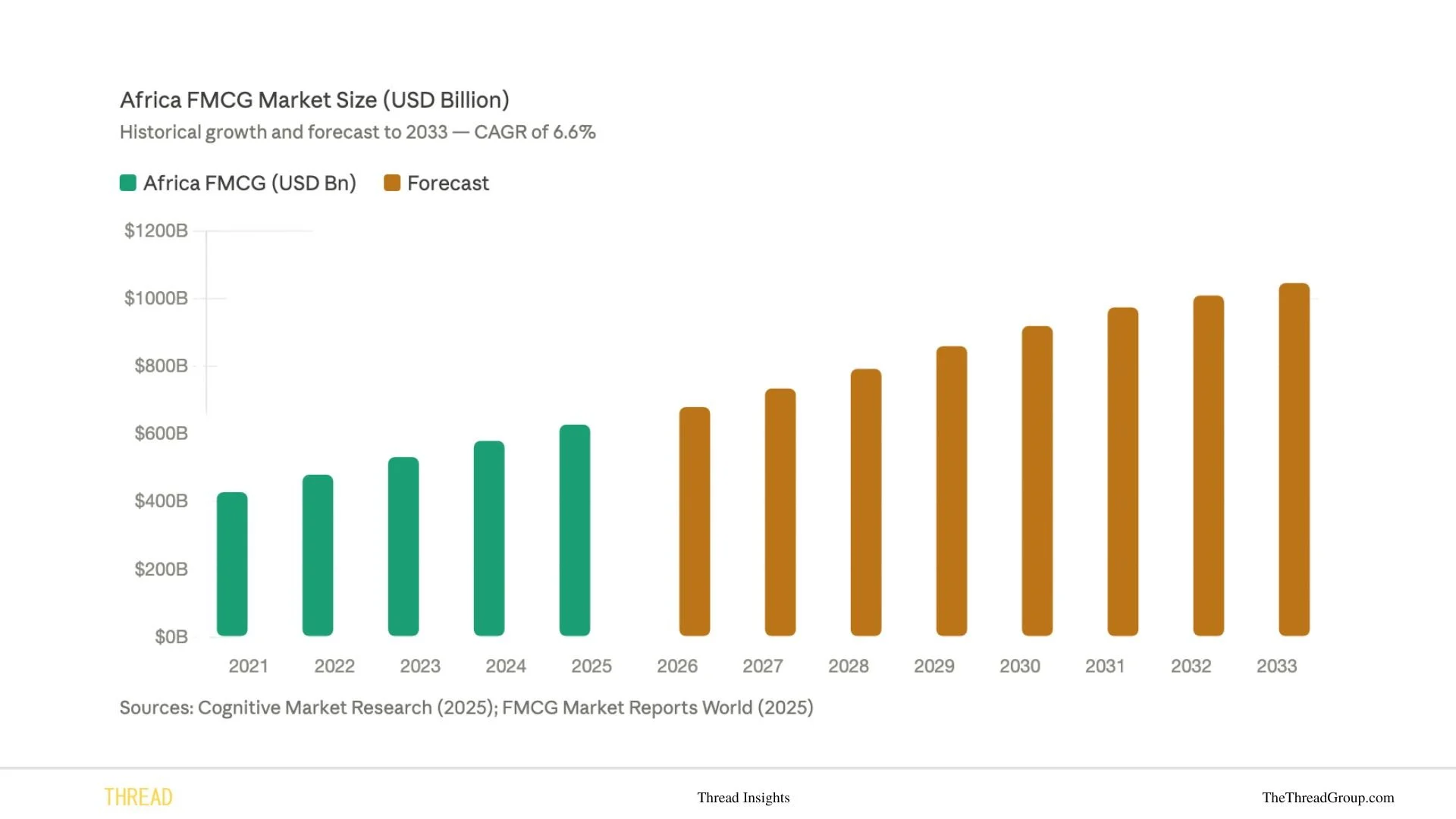

Africa's FMCG industry grew from $428.5 billion in 2021 to $628 billion in 2025, and is projected to reach $1.047 trillion by 2033 at a CAGR of 6.6%. Cognitive Market Research To put that number in perspective, the entire continent's FMCG sector will more than double in under a decade. This is not speculation. It is the arithmetic of demographics, urbanization, and a rising middle class playing out in real time.

Middle East and Africa is currently the fastest-growing FMCG region in the world, with a projected CAGR of 5.98% through 2033, outpacing North America and Europe. SNS Insider

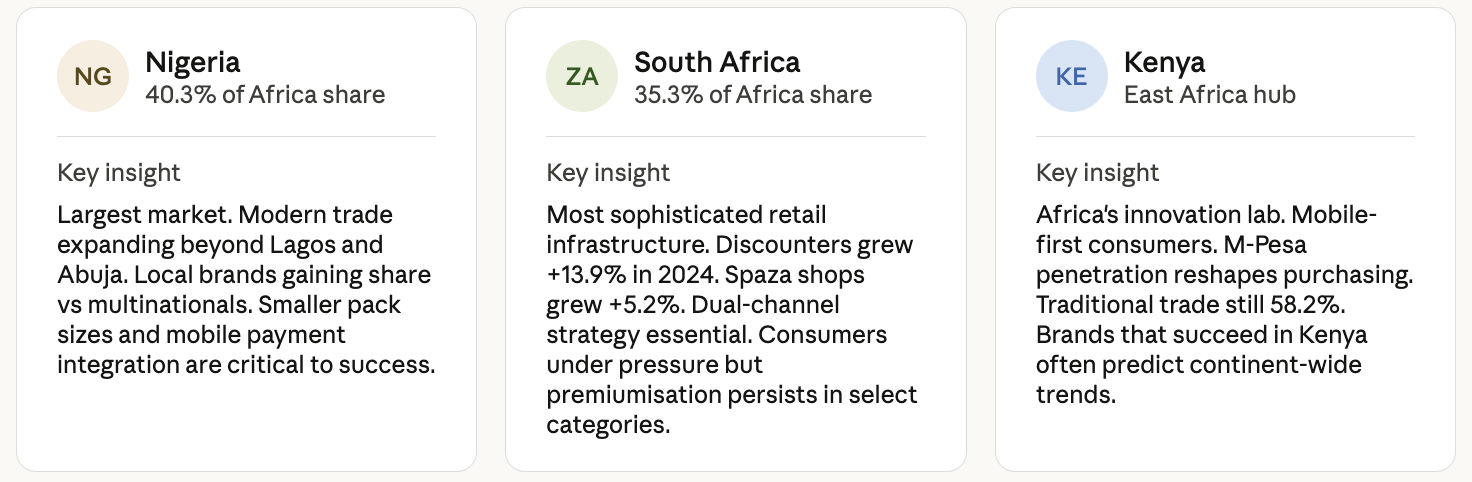

Within Africa, two countries currently dominate. Nigeria holds 40.3% of Africa's FMCG market share, while South Africa holds 35.29%. Cognitive Market Research Together they represent three quarters of the continent's formal FMCG economy — but they are also where the hardest lessons about how to operate in this market have been learned.

Why Africa's Consumer Market Is Unlike Any Other

Anyone who approaches Africa's FMCG sector with a cut-and-paste strategy from Europe or the Americas will lose money, time, or both. The structural realities here are fundamentally different, and they create both the friction and the opportunity.

The Informal Trade Is Not a Gap in the Market. It Is the Market.

South Africa alone has as many as 200,000 spaza shops, spazarettes, superettes, midi wholesalers, and hawkers. As much as 40% of total food bought by consumers each year comes from these informal traders, who service 77% of the population. IOL

Growth in the informal retail space was up 5.2% in 2024, with proximity and convenience continuing to drive shopper loyalty. Spaza shops and township outlets retained relevance particularly for small, frequent shopping missions and cash-based shoppers. Trade Intelligence

This creates a paradox that any FMCG brand entering this market must reckon with: you can build a product that wins on supermarket shelves and still miss the majority of your potential consumers. The Dyula traders understood this centuries ago. They went where the people were, not where the infrastructure was easiest.

The African continent is dominated by traditional retail that is not as prevalent elsewhere. These are mostly unlicensed or unregistered retailers operating in kiosks or street-side stalls, making localized distribution strategies crucial for FMCG brands. BeatRoute

Understanding the Pricing Reality

African consumers, particularly those away from large metropolises, prefer to spend primarily on essential goods because of low average incomes. But there has been a steady rise in disposable income in areas with steady economic and political conditions, meaning the sale of personal care and premium products is rising. BeatRoute

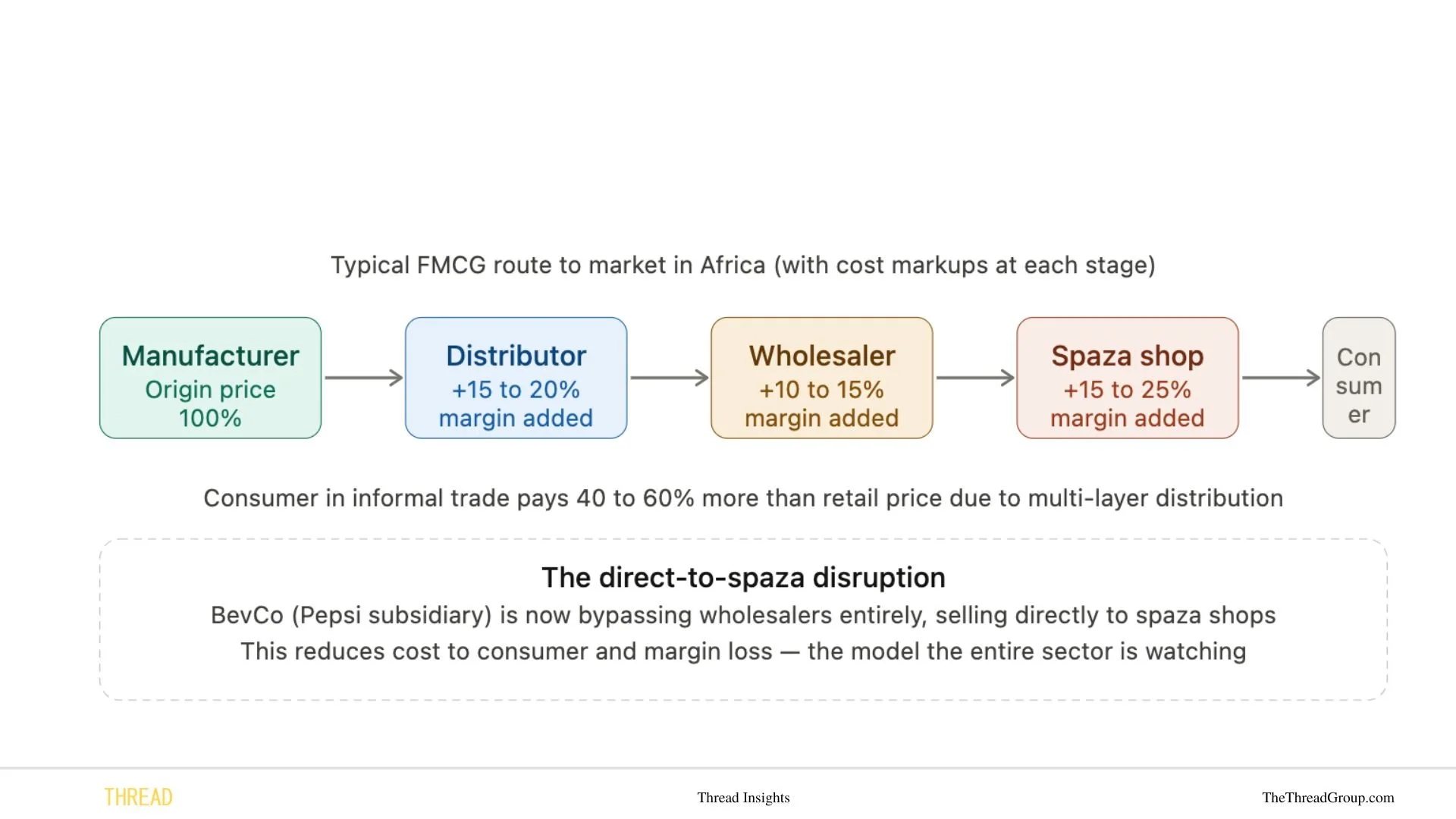

Spaza store owners and informal traders face challenges including inefficient supply chains resulting in product stockouts, high waste due to limited shelf life of fresh produce, increased dependency on the sale of overpriced branded products, and little buying power. Unlike supermarkets that buy direct from FMCG brands, most spaza shops purchase stock from wholesale retailers and add their own markup, meaning goods are more expensive and the shop relies on convenience as its primary driver. Bizcommunity

This means a product can actually be more expensive to buy in a township spaza than in a Johannesburg supermarket, despite the township consumer having less disposable income. That structural inefficiency is one of the biggest unresolved problems in African FMCG, and it is also one of the biggest opportunities for anyone clever enough to solve it.

The Digital Revolution That Is Rewriting the Rules

If the Dyula traders were operating today, they would be on their phones.

According to the GSMA, mobile penetration across the continent reached 495 million unique subscribers by 2024, representing 46% of the total population. 4G coverage now exceeds 65%, and smartphone adoption is expected to surpass 73% by 2025. African Exponent

Mobile money services grew by 12% year-on-year in 2023, reaching a transaction value exceeding $500 billion. Platforms like M-Pesa, Flutterwave, and Paystack are transforming how consumers pay for everyday goods. Worldecomag

Africa has the youngest population in the world, with 70% of sub-Saharan Africa under the age of 30. These urban youth are driving tech adoption and reshaping retail, entertainment, and food consumption. Marketinganalytics

This demographic reality is the single most important fact about the African FMCG market. A continent where the median age is under 20 is a continent of first-time consumers, first-time buyers, and first-time brand loyalties being formed right now. Whoever wins the trust of these consumers in the next decade will hold it for the next half century.

M-Pesa and the Transformation of Commerce

The story of how mobile payments reshaped consumer goods purchasing in East Africa is the most important recent case study in African FMCG. Kenya's M-Pesa, launched in 2007, did not just change how people paid. It changed what they could buy, where they could buy it, and from whom. By removing the friction of cash-only transactions from informal retail, it enabled a new generation of micro-merchants to stock FMCG products they could not previously afford to hold in inventory.

M-Pesa processed over $364 billion in transactions in 2023, serving over 60 million users across seven countries. African Exponent

Kenya serves as an innovation hub for African retail. Consumer behavior insights in Kenya often predict trends that spread across the continent. Mobile money adoption started there and transformed shopping behaviors, influencing retail operations throughout East Africa and beyond. Novatia Consulting

Nigeria stands as the largest market in Africa for mobile payments, holding 25.4% of the regional market. The Africa mobile payments market was valued at $75.22 billion in 2025 and is expected to grow at a CAGR of 39.3% through 2034. Market Data Forecast

Country Deep Dives: Where the Battles Are Being Fought

South African consumers spent R214 billion on FMCG and Technology and Durable products in Q3 2024 alone, representing year-over-year growth of 4.1%. NielsenIQ

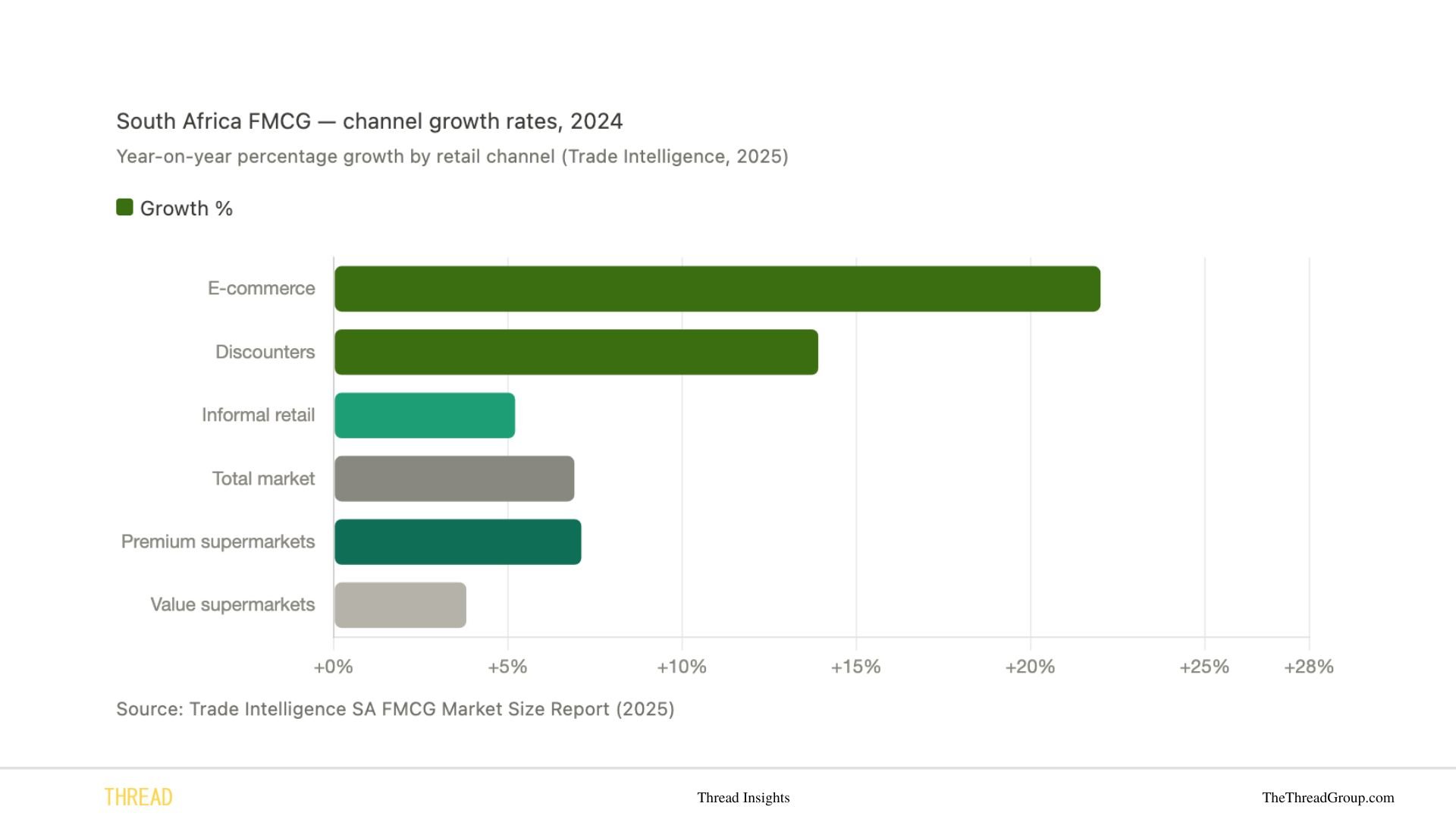

Total FMCG retail sales in South Africa grew 6.9% in 2024, with performance supported by footprint expansion in the corporate retail sector, interest rate cuts, and early retirement withdrawals under the two-pot system. Trade Intelligence

In Kenya, traditional trade still dominates the retail landscape with a 58.2% contribution in 2023, while modern trade contributed 41.8%. Beverage, ambient food, and dairy categories consistently lead value growth. NielsenIQ

The Five Forces Shaping the Future of African FMCG

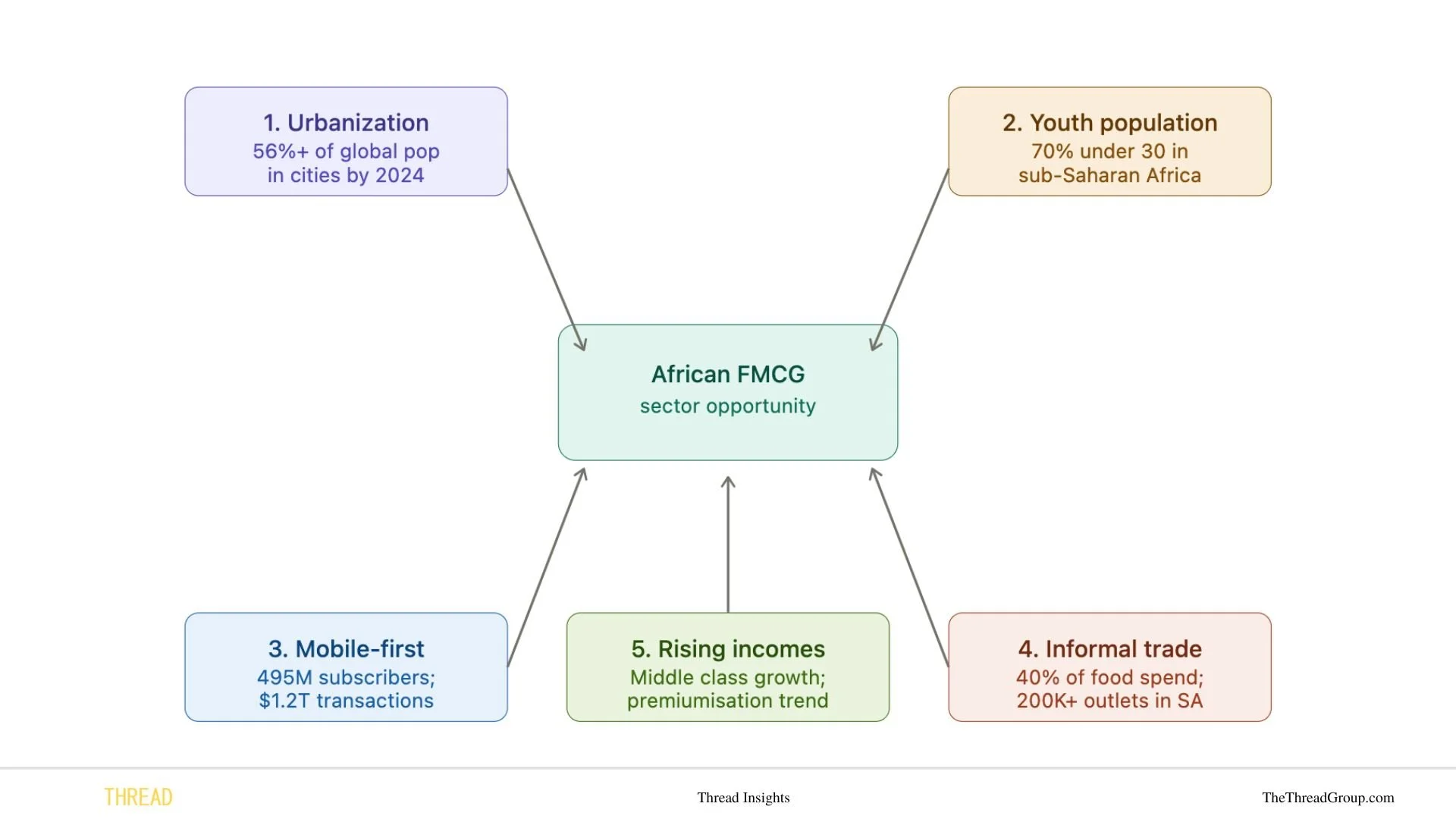

Force 1: Urbanization and the Packaged Goods Shift

Over 56% of the global population lived in urban areas by 2024, up from 52% in 2020. Urban households consume 35% more FMCG products than rural households. Marketreportsworld In Africa, this shift is happening faster than anywhere else on earth. Lagos is on trajectory to become the world's most populous city by 2100. Nairobi, Accra, Addis Ababa, and Dar es Salaam are all experiencing double-digit annual urban growth. Every person who moves from a rural area to a city trades a subsistence economy for a packaged goods economy. That transition represents a new FMCG consumer, every single time.

Force 2: The Youth Dividend

Africa's median age is approximately 19. The continent's 1.4 billion people will grow to over 2 billion by 2050, and the overwhelming majority of that growth will be young people. These are consumers who have grown up with mobile phones, social media, and aspirational brands. They are not loyal to legacy brands by default. They are forming their brand relationships right now. Young consumers in Nigeria, who represent over 60% of the population, drive demand patterns and respond strongly to digital engagement and mobile payment adoption. Novatia Consulting

Force 3: The Mobile Money Infrastructure

The Dyula trader's distribution network was built on trust and physical roads. Today's equivalent is mobile money infrastructure, and Africa has built the world's most sophisticated version of it. In Nigeria, the Central Bank's Instant Payment system linked to mobile money platforms enabled businesses to transact instantly across banks and mobile networks, leading to a 30% increase in B2B mobile transfers in 2023. Market Data Forecast This infrastructure is the missing link between manufacturers and the informal trade, and companies that crack this connection gain a decisive competitive advantage.

Force 4: The Informal Trade Unlock

The informal independent sector in South Africa represents R178 billion, effectively fed through different channels and routes to market depending on where traders buy from. FMCG suppliers have not yet fully tapped this market because of supply chain challenges. Bizcommunity

But technology is beginning to bridge this gap. Yebofresh has created an e-commerce platform that links township entrepreneurs with high-quality goods and services, currently serving 6,000-plus businesses in more than 25 townships with 24-hour delivery and buy-now-pay-later offerings. Vuleka has designed a fintech app tailored to the needs of spaza shop owners, structuring it to support an entire trading system within the informal sector. Bizcommunity

Force 5: Premiumization Amid Pressure

Here is the apparent paradox: African consumers are simultaneously under financial pressure and moving toward premium products. Both statements are true, for different consumer segments. Premium supermarkets outperformed value supermarkets in South Africa in 2024, reflecting a bifurcated market where some consumers traded up while others sought out discounters. Trade Intelligence The FMCG brand that can serve both ends of this spectrum, or pick its lane with precision, is the one that wins.

The Distribution Problem: Africa's Biggest FMCG Challenge

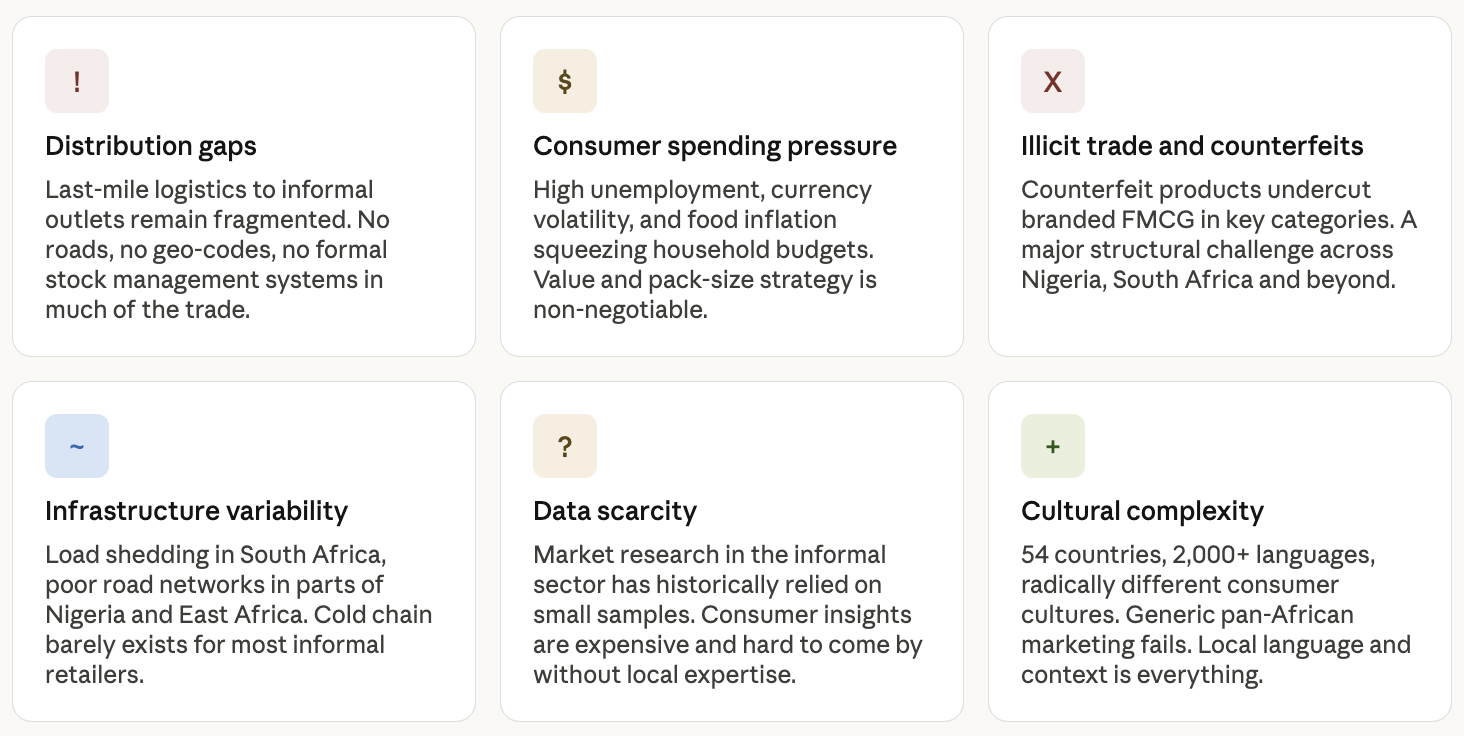

The distribution challenge is the defining operational problem of African FMCG. The lack of infrastructure, storage space, and the reluctance to keep stock on site due to the threat of crime has created a channel that requires high-touch, frequent stocking. Expecting a spaza owner to buy once a month to take advantage of bulk pricing is not realistic. These outlets want to see stock moving off their shelf every day. Retail Brief Africa

A more interesting development in South Africa is the realisation of the size of the informal trade in townships, which runs into billions of rands. Advancements in logistics, technologies for stock management and distribution, and deeper market insights with the help of AI have the big retailers and manufacturers taking township spaza shops seriously. BevCo, a subsidiary of multinational Pepsi, is now selling directly to spaza shops, bypassing wholesalers and saving on distribution costs. Who Owns Whom

This model, direct-to-spaza, is the innovation the sector has been waiting for. The brands that execute it first and at scale will own the most important last-mile distribution network on the continent.

The Geography Problem

Even if FMCG businesses wanted to nurture a direct business relationship with spazas, these shops are usually based in townships, some with no roads or geolocation codes, making it difficult for suppliers to understand the number of stores available as a starting point for serving them. BeatRoute

Companies like 5M2T have tackled this directly: they visit over 60,000 geo-located spaza outlets per month in all major provinces, serviced daily by trained staff. This has succeeded where more formalized distribution networks previously failed due to on-the-ground understanding of the complexity of the informal market. Retail Brief Africa

What the Data Says About Consumer Behaviour Right Now

E-commerce remains the fastest-growing channel in South Africa's FMCG market, while discounters such as Boxer, Usave, and SaveMor recorded high year-on-year growth of 13.9%. Both are growing from a smaller base, but the trajectory is unambiguous. Trade Intelligence

FMCG companies are increasingly turning to technology solutions, including AI, to better understand consumers and reduce costs. Trends include consumers buying down, growing contribution of online sales, and increasing focus by retailers and producers on selling to informal traders. GlobeNewswire

Buying Down and the Pack Size Revolution

One of the most practically important trends in African FMCG right now is "buying down," which means consumers shifting to cheaper alternatives or smaller pack sizes rather than stopping purchases entirely. The rising cost of living continues to halt volume growth in some markets. Consumers are rationalizing their purchases by spending more for less. Manufacturers and retailers must continue to innovate products, exploring better value-for-money options that can still meet the needs of the already-stretched consumer. NielsenIQ

Smaller pack sizes are not just a concession to poverty. In the informal trade, they are the entire model. A consumer who earns daily cannot buy a week's supply of washing powder. She buys one sachet. The brand that offers the right sachet at the right price point at the right spaza shop will win her lifetime loyalty.

The Health and Wellness Shift

In an informal shopper survey conducted for Trade Intelligence, 68% of shoppers said they purchased more fresh produce, fruits and vegetables, in 2020 from their local spaza shops than the year before. IOL This trend toward health awareness has only accelerated since then. Across the continent, urban consumers are increasingly demanding products with health credentials, functional benefits, and transparent ingredients. Personal care grew fastest in the FMCG market at a 5.62% CAGR, while food and beverages led with a 41.27% market share. SNS Insider

The Critical Challenges: What Stands Between You and Success

Poor logistics and infrastructure and illicit trade have held back FMCG growth in South Africa, while FMCG companies' expansion into the broader continent has slowed due to logistics and currency challenges. GlobeNewswire

The data scarcity problem is particularly underappreciated. Most formal market research in Africa concentrates on urban consumers in modern trade. The majority of actual consumption happens in a channel that is poorly mapped, poorly measured, and poorly understood. Market research in this sector has always been based on small sample sizes extrapolated without understanding the spatial distribution, neighbourhood market sizes, and varying degrees of formalization that exist within the sector. Retail Brief Africa

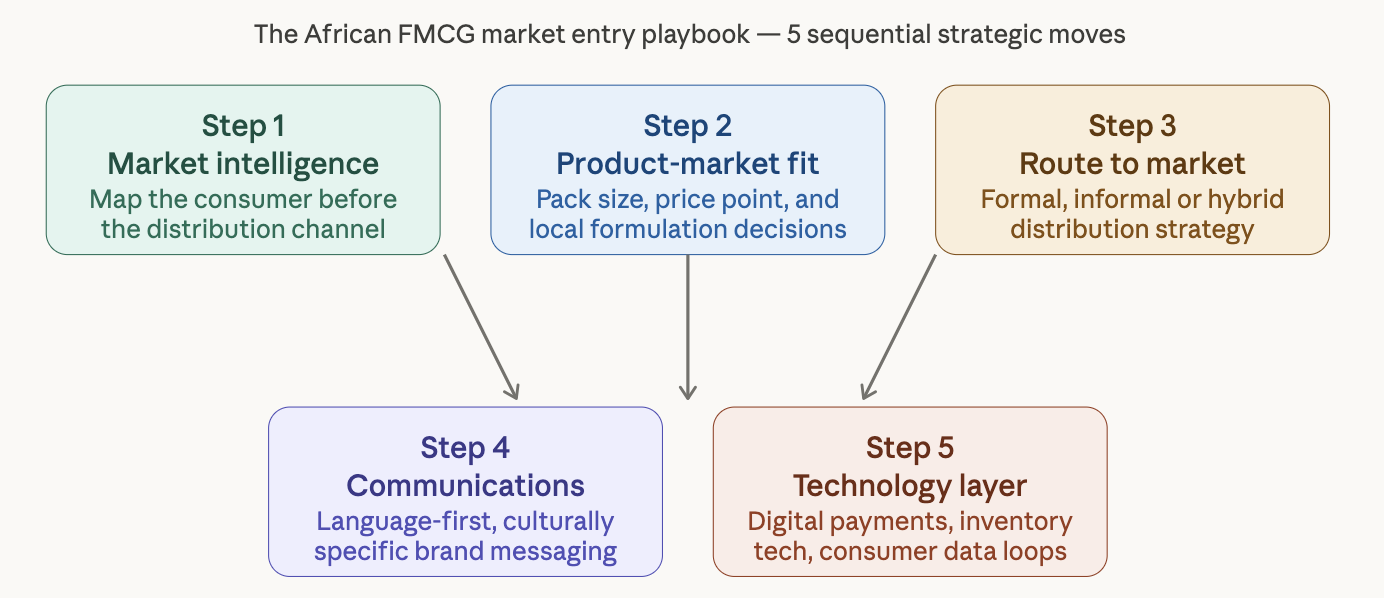

A Practical Playbook: How to Enter and Win in African FMCG

The following framework is drawn from the operational realities of the market. It is not theoretical. It is what the companies actually winning in this sector are doing.

Step 1 — Know Your Consumer Before You Know Your Channel

The single biggest mistake foreign FMCG entrants make in Africa is prioritizing distribution logistics over consumer understanding. You can build the most efficient distribution network on the continent and still fail because you are delivering the wrong product to the wrong segment at the wrong price. Market intelligence is not a phase you go through before the real work starts. It is the real work.

Specific questions to answer before entering any African FMCG market: What is the actual household income profile in your target area? What does the daily purchasing rhythm look like? Is the consumer buying weekly, daily, or per meal? What role does brand trust play versus price sensitivity? What language does she think in when she evaluates a product?

Step 2 — Product-Market Fit Is Not Optional

Pricing strategies must reflect local economic realities. Nigeria's market responds well to smaller pack sizes and affordable price points. South Africa's market supports premium positioning for products that demonstrate clear value. Novatia Consulting

Successful FMCG companies in Africa reformulate, resize, and reprice their products specifically for each market. Not as an afterthought, but as the starting point of their product strategy. This is what the Dyula traders knew: a kola nut that sells in Kumasi needs different handling than one that sells in Timbuktu.

Step 3 — Distribution Is a Competitive Advantage, Not a Commodity

The most defensible moat an FMCG brand can build in Africa is a distribution network that reaches the informal trade directly. FMCG brands in Africa are investing in technology toward improving both customer service and gathering critical information to support seamless route-to-market operations. Cadbury, for example, equips its sales teams in South Africa with mobile devices enabling them to audit inventory and place orders efficiently. BeatRoute

Step 4 — Communications Must Speak the Market's Language

Africa is not a country. It is 54 countries with over 2,000 languages, profoundly different cultural contexts, and deeply varied consumer values. The brand that treats "Africa" as a monolithic market in its communications will fail to connect with almost everyone. For example, the rise of mobile apps and digital services in Nigeria has created new platforms for brands to engage with tech-savvy youth. By aligning branding with youth culture, businesses can capture this influential market. Marketinganalytics

The communications challenge in Africa is not about translation. It is about cultural fluency. A product communication that works brilliantly in Lagos may be tone-deaf in Cape Town and incomprehensible in Nairobi. This is not a problem that can be solved with a global agency brief. It requires people who understand the cultural codes of the specific market.

Step 5 — Build Your Technology Layer from Day One

FMCG companies are increasingly turning to technology solutions, including AI, to better understand consumers and to reduce costs. GlobeNewswire

The technology opportunity in African FMCG is not about making things more efficient for large corporations. It is about making things possible for the first time. Stock management systems that work on a feature phone. Payment solutions that function without reliable internet. Consumer insight tools that reach informal trade outlets. These are the technology gaps that, when solved, unlock the market.

The Opportunity Ahead: Why Now Is the Critical Moment

Bringing It Together: What the Dyula Knew and What You Need Now

Return to our Dyula trader for a moment. What made him successful across centuries and thousands of miles of hostile terrain?

He knew the consumer. He understood the distribution challenge as the core problem to solve. He built trust-based networks that substituted for formal infrastructure. He was linguistically and culturally fluent in every market he entered. And he used the technology of his time, which was credit, relationships, and route knowledge, to create advantages that his competitors could not replicate quickly.

None of that has changed. The scale has. The speed has. The technology has. The consumer's expectations have evolved dramatically. But the fundamental strategic imperatives are identical.

Africa's FMCG sector is now at an inflection point that only comes along once or twice in a generation. Local brands in Africa and Asia are already capturing over 30% of market share in categories like snacks and personal care. Marketreportsworld The window to build category-defining brands, distribution networks, and consumer relationships is open. It will not stay open indefinitely.

The question is not whether to enter the market. The question is whether you have the right team, the right intelligence, and the right tools to do it well.

Finding Your Edge in Africa's FMCG Market: The Thread Group

The data is clear. The opportunity is real. But reading a market report and knowing how to move in a market are two entirely different things.

Africa's FMCG sector rewards those who invest in genuine understanding before they invest in action. The brands, investors, and entrepreneurs who win here are not necessarily the ones with the biggest budgets. They are the ones who knew something their competitors did not, and who used that knowledge to make smarter decisions faster.

That is where we come in.

Thread Strategy is the research and business development arm of the group. For FMCG players, this means getting the kind of market intelligence that actually shapes strategy: consumer behaviour research in formal and informal trade, channel mapping, competitive landscape analysis, and business development support for brands entering new African markets or scaling existing operations. If the article above raised more questions than it answered for you about your own market position, Thread Strategy is where those questions get resolved.

Thread Studio handles the communications challenge that the article identifies as one of the sector's most underestimated risks. Speaking to African consumers is not a translation exercise. It is a cultural fluency exercise. Thread Studio develops brand communications that are built from the inside out, in the language and cultural context of the specific market you are entering, not adapted from a global brief. In a sector where consumer trust is built at the neighbourhood level, this is not a nice-to-have. It is the difference between a brand that resonates and one that does not get past first purchase.

Whether you are a multinational looking to deepen your African market intelligence, a local brand ready to scale, an investor evaluating an FMCG opportunity, or an entrepreneur building something new in this space, the Thread Group is structured to meet you where you are.

The Dyula traders who built their trade networks across the continent six centuries ago did not do it alone. They built coalitions of expertise, trust, and local knowledge. The principle still holds.

Contact us today at Clients@thethreadgroup.com